During the five-month period from November to March, the S&P rose 24%, reflecting confidence that inflation was finally on the decline, prices could get under control, and interest rates would be reduced. Unfortunately, that confidence was misplaced. Instead, through the early part of this year we are seeing several reflationary signals. Prices are accelerating upward again due to faster job growth, strong consumer spending, higher oil prices, and continually rising housing costs.

Consequently, Q2 is off to a challenging start. With stocks down over 5% so far in April, the S&P is tracking towards its worst calendar month since December 2022. At this point, two seemingly conflicting events appear to be occurring. On one hand, the odds of a recession hit a 2-year low earlier this month.

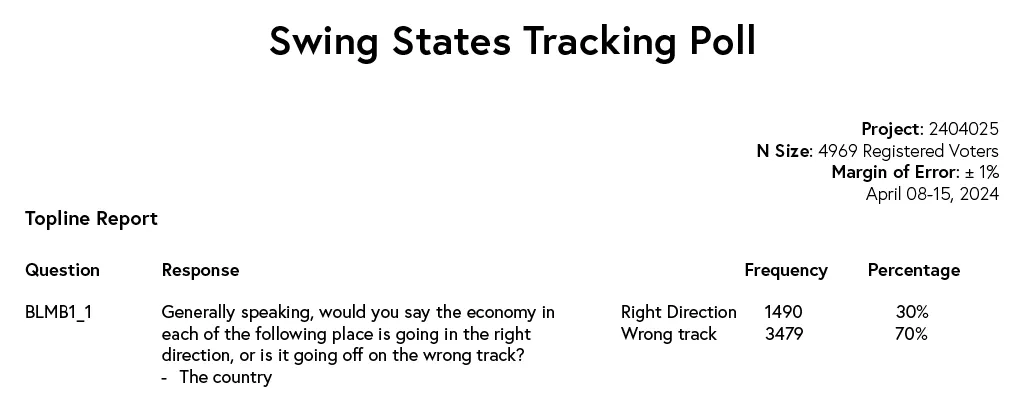

On the other hand, 70% of Americans believe the US economy is going the wrong direction. So what gives?

Many economists have observed that the US is experiencing a major bifurcation of the economy. There are those who have benefited from higher interest rates – individuals who own significant assets such as homes and stock portfolios have seen a boost in personal wealth from favorable financial conditions that allowed them to lock in low-cost debt and see their stock and real estate portfolios surge. At the same time, most other American consumers are being squeezed by higher rents, more expensive credit card and auto debt, and elevated living expenses.

Nancy Lazar, Piper Sandler’s chief global economist, remarked that such bifurcation is unusual and occurred only during the energy crisis in 1978-1979 and the Great Recession in 2008. She commented, “At the end of the day, the interest rate structure had to go higher for longer, and in turn, eventually, you did have a recession, and that’s how you eventually crushed the excesses and inflation.”

In response to the recent economic data, we have seen the Fed turning decidedly more hawkish. In his recent speech in Washington, D.C., Fed Chair Jerome Powell acknowledged the recent “lack of progress” in reaching the central bank’s inflation goal and expressed a willingness to “maintain the current level of [interest rates] for as long as needed.”

The futures market has drastically reduced its expectation of rate cuts since the start of the year, and some investors have gone further to suggest the Federal Reserve’s next move might actually be a rate hike instead of a reduction. Option markets are now pricing in a roughly one-in-five chance of a US rate increase over the next 12 months. This sentiment echoes comments from former US Treasury Secretary, Lawrence Summers. He said in a recent interview, “You have to take seriously the possibility that the next rate move will be upwards rather than downwards,” indicating he believes the likelihood is between the 15% – 25% range.

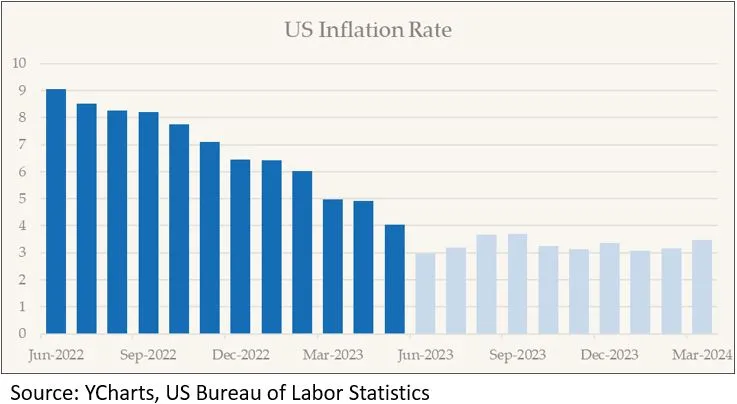

Between March 2022 and July 2023, the Federal Reserve raised interest rates 11 times by a total of 5.25%. That period coincides fairly closely with the period of disinflation that saw price growth decline from 9% in June 2022 to around 3% in June 2023.

The Fed’s willingness to hold rates steady since then and even signal the possibility of cutting rates has halted progress on reaching the Fed’s 2% inflation goal. In fact, since last June, inflation has actually gotten worse—rising from 2.97% to 3.48% over the last nine months.

At the same time, while inflation has picked up, economic growth is starting to slow down. Inflation-adjusted GDP rose just 1.6% in Q1, way below a 2.4% forecast from economists and the 3.4% growth rate seen in Q4. A couple of key factors drove the decline.

First, US exports and business inventories grew more slowly. Most economists recognize that these categories can be volatile and do not necessarily reflect the overall health of the economy.

Second, government spending increased at its lowest rate in nearly two years, rising just 1.2% compared to 4.6% last quarter. Much of the recent growth has been propped up by numerous infrastructure and clean energy projects driven by federal legislation.

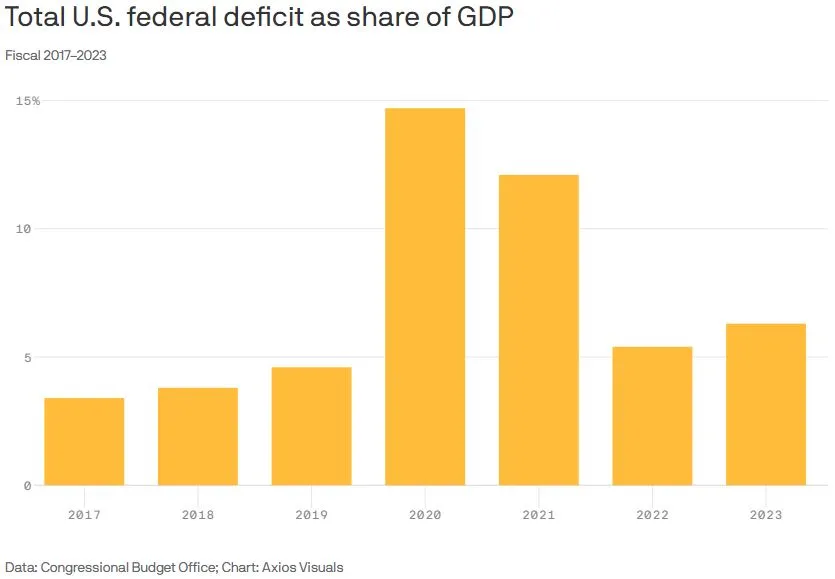

That high level of recent Federal spending has drawn criticism from the International Monetary Fund (IMF). The global financial agency said this month that the US’s loose fiscal policy and record public spending and borrowing is “out of line with long-term fiscal sustainability.” Last year the US fiscal deficit equaled 6.2% of GDP. That is more than double the 3% maximum guideline of the European Union, which it has far exceeded for several consecutive years.

The fastest growing source of the increased spending is coming from servicing more debt at higher rates. In 2023, the US paid over $1 trillion to service its debt—more than it spent on Defense, Medicare, or Medicaid.

With debt forecasted to grow from about $34 trillion to $54 trillion over the next decade, these costs will not likely decrease soon. This year, the outstanding federal debt is expected to exceed 100% of GDP for the first time in the country’s history.

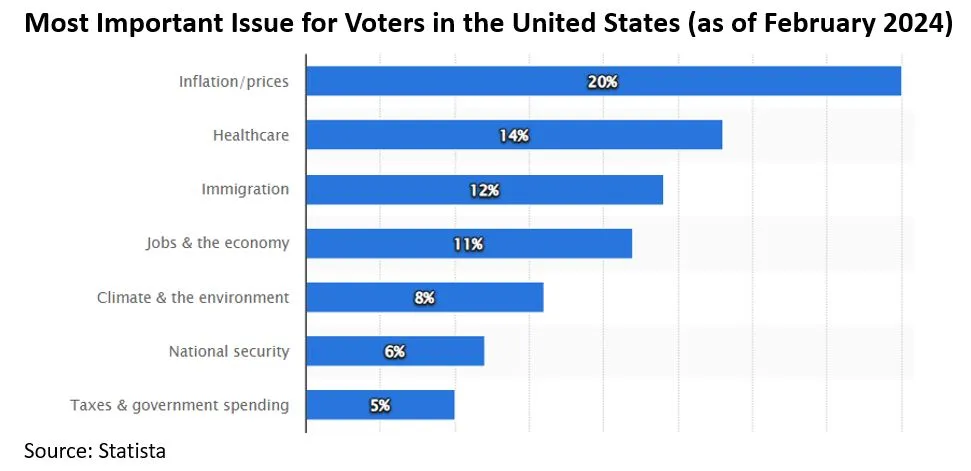

These issues will be weighing on voters’ minds as we approach this fall’s presidential election. Concern about inflation remains the top issue for voters, followed by the US health care system and immigration.

While loose fiscal policy has made tackling inflation more difficult, it has helped the US economy stave off a recession thus far. Another contributing factor is an influx of immigration, which now exceeds pre-pandemic levels.

The US Congressional Budget Office (CBO) estimates immigration will boost GDP by $7 trillion over the next decade and raised its estimate of the size of the labor force by 5.2 million people by 2033. While the CBO expects the larger population to boost spending, productivity, and stabilize wage growth, there is considerable concern that the bulk of the increased migration is coming from people entering the country illegally.

This economic resilience is also causing the US economy to grow faster than its foreign rivals. According to the IMF, this year the US is expected to account for 26.3% of global GDP, which would be its highest share in nearly two decades. Europe’s contribution has dropped by 1.4%, Japan by 2.1%, and even China’s economy has slipped in comparison to the US since 2018.

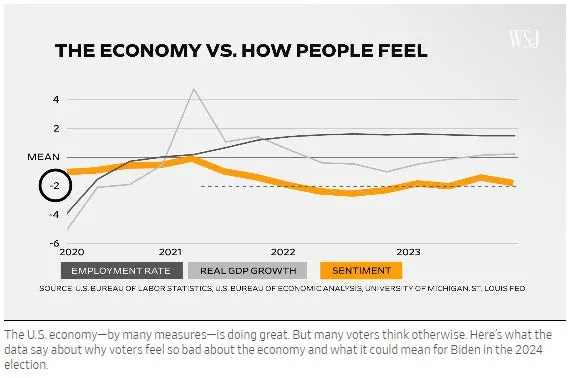

Likely more influential on the election than the US economy is voter perception of the economy. Although unemployment and economic growth, two major indicators of economic health, have both performed above historical averages, US sentiment about the economy is around two standard deviations below its average.

While many economists view the current state of the US economy more positively, consumers continuing to feel the burden of inflation feel differently. Inflation continues to shape public perception, and consumer sentiment has tended to be a strong predictor of elections. More recently, however, consumer sentiment has started to improve. In the coming months, economists as well as political scientists will be playing close attention to inflation and economic indicators not just for the sake of the economy, but for the sake of future US leadership.